Stablecoins - Stability in a Volatile World

Stablecoins offer a bridge the gap between fiat currencies like the U.S. dollar and cryptocurrencies.

(Any views expressed in the below are the personal views of the author and should not form the basis for making investment decisions, nor be construed as a recommendation or advice to engage in investment transactions.)

What are they?

Stablecoins are fiat-backed digital currencies with reserves held in regulated financial intuitions and redeemable in local currencies through the traditional banking system. In short, they are merely a digital native wrapper for commercial bank dollars. No new money is being created. Instead, stablecoins are a representation of value leaving the commercial banking system and shifting into the public blockchain ecosystem. Stablecoins are useful for transactions in DeFi as they introduce a vehicle of stable value vs the volatility associated with bitcon, ether, or other cryptocurrencies. Stablecoins are the most crucial element of Defi and have received the most attention from regulators - regulatory visibility is likely right around the corner. Because public blockchains are less encumbered than established payment networks, stablecoins can cater to a wider variety of end users who might otherwise be excluded from the financial system

What are they used for?

Stablecoins are used globally to facilitate trading, lending, or borrowing of other digital assets, predominantly on or through digital asset trading platforms. For example, individuals and institutions that actively trade cryptocurrency will make one-time, or periodic deposits of fiat from their bank account onto a crypto brokerage platform and then convert the fiat dollars into a stablecoin that can be used at any time to buy crypto assets. In addition, traders can sell crypto assets and receive proceeds in the form of a stablecoin. Stablecoins reduce the need / dependence on traditional financial institutions, for now. Lastly, stablecoins have seen strong adoption in emerging markets with currencies undergoing hyper devaluation (i.e., Turkey, parts of the Middle East, Africa, and Latin America)

What are they backed by?

The short answer is, it depends. Broadly speaking there are four common types of stablecoin collateralization schemes: i) fiat-collateralized, ii), commodity-collateralized, iii) crypto collateralized, and iv) algorithmic stablecoins

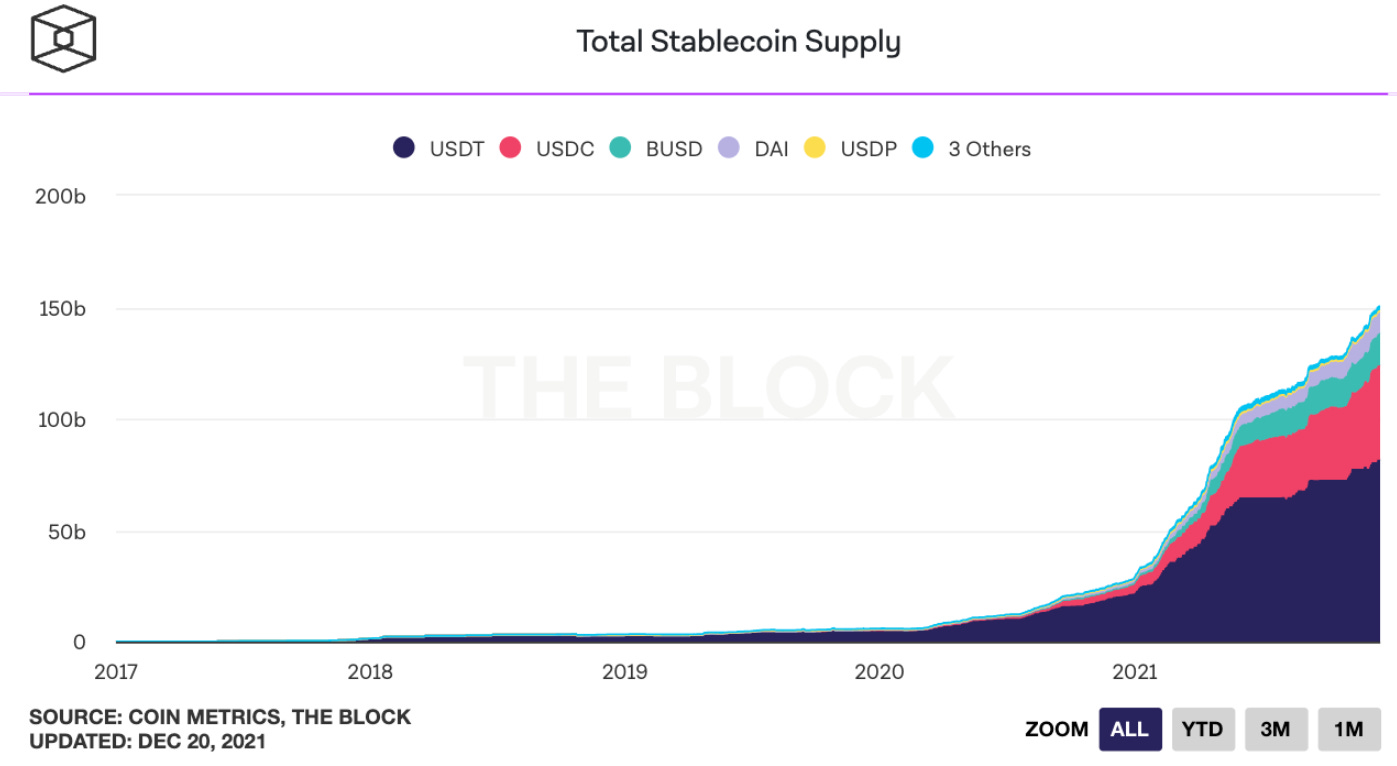

Fiat-collateralized (90%+ of stablecoin market value)

Fiat backed stablecoins are the simplest and most commonly used stablecoins. Issuers of fiat-collateralized stablecoins deposit dollars into a bank account and issue stablecoins 1:1 against those dollars. When a user wants to liquidate their stablecoins back to USD, the issuer destroys the stablecoin and wires them the USD. It is important to note that majority of stablecoin issuers have to register with FinCen, obtain money transmitter licenses on a state by state basis, and maintain stable bank and audit relationships. They generally speaking, are regulated entities, which is counter to the mainstream narrative that stablecoins are unregulated. Instead, the mainstream narrative is really about transparency and determining what institutions should have the power to issue stablecoins. More on this below

The benefits of fiat-backed stablecoins are 100% price-stable (i.e. there is no fluctuation in the value of the underlying reserves) and they are generally safe as no collateral is held on a blockchain and is instead custodied via the legacy banking system. The pitfalls are they can be expensive and slow to liquidate back into fiat and require centralization and trust that the reserves are in the form and quantity that the issuer claims they are. The most commonly used fiat-collateralized stablecoins are Tether ($USDT), USD Coin ($USDC), and Paxos ($PAX)

Commodity-collateralized

Commodity-backed stablecoins are collateralized using physical assets like precious metals, oil, and real estate. The most popular commodity to be collateralized is gold. Commodity-backed stablecoins facilitate investments in assets that may otherwise be out of reach locally. For instance, in many regions, obtaining a gold bar and finding a secure storage location is complex and expensive. Tether Gold (XAUT) and Paxos Gold (PAXG) are two of the most liquid gold-backed stablecoins

Crypto-collateralized

Crypto-collateralized stablecoins hold crypto assets such as ether (ETH) in escrow for the issuance of new stablecoins. Given the reserve assets are crypto native, users have the ability to access crypto-collateralized stablecoins without needing to utilize or trust a centralized party. However, the biggest drawback with this arrangement is that crypto-collateralized stablecoins often require over-collateralization to account for price volatility. For example, in order to receive $100 of a crypto backed stablecoin, you will need to put at least $150 worth of ETH as collateral. This is a major drawback compared to fiat-collateralized stablecoins which are merely backed 1:1. Maker Dai ($DAI) is the most common crypto-collateralized stablecoin

Algorithmic

Algorithmic stablecoins do not use fiat or cryptocurrency as collateral. Instead, their price stability results from the use of specialized algorithms and smart contracts that manage the supply of tokens in circulation. An algorithmic stablecoin system will reduce the number of tokens in circulation when the market price falls below the price of the fiat currency it tracks. Alternatively, if the price of the token exceeds the price of the fiat currency it tracks, new tokens enter into circulation to adjust the stablecoin value downward

Regulatory Showdown

In November 2021, the Presidents Working Group on Financial Markets issued a report on stablecoins. If you want to know the details of where decision makers in Washington are focused it’s a worthwhile read. In short, the working group identified three primary risks in the current stablecoin market:

Investor Protection: Speculative digital asset trading, which may involve the use of stablecoins to move easily between digital asset platforms or in decentralized finance (DeFi) arrangements, present risks related to market integrity and investor protection. These market integrity and investor protection risks encompass possible fraud and misconduct in digital asset trading, including market manipulation, insider trading, and front running, as well as a lack of trading or price transparency

Illicit Activity: Stablecoins pose illicit finance concerns and risks to financial integrity, including concerns related to compliance with rules governing anti-money laundering and countering the financing of terrorism

Trust: If stablecoin issuers do not honor a request to redeem a stablecoin, or if users lose confidence in a stablecoin issuer’s ability to honor such a request, runs on the arrangement could occur that may result in harm to users and the broader financial system

The paper proposes the following solutions:

To address risks to stablecoin users and guard against stablecoin runs, legislation should require stablecoin issuers to be insured depository institutions (i.e. US Banks), which are subject to appropriate supervision and regulation, at the depository institution and the holding company level

Should require custodial wallet providers oversight

legislation should require stablecoin issuers to comply with activities restrictions that limit affiliation with commercial entities

In short, the guidance from the presidents working group is that to increase investor protection, market stability, and government oversight, stablecoin issuance should only be allowed by Banks.

Hot take / so what?

One of the inhibitors to continued broad-based crypto adoption is the lack of clarity in the regulatory framework. I take is as a major step in the right direction that Washington is putting time and resources into determining the right regulatory framework for various parts of the Digital Asset ecosystem. Clarity on the issuance and oversight of stablecoins will accelerate adoption. In addition, I think it is not if, but when will US regulated banks become the primary issuer of stablecoins - another boon for continued adoption and potentially an accelerate to the improvement of existing payment rails

To me, the non-obvious benefactor of stablecoin adoption and growth is the US. Stablecoins represent a massive unlock for access to dollars. There exists significant demand across the globe for US dollars. Particularly in nations dealing with hyperinflation and people exposed to monetary repression through forced devaluations or expropriation. While the US has an inflationary currency, it is the least inflationary of the lot. Today, if you live in a place like Venezuela, the challenge is that US dollars are incredibly scarce because the traditional, brick and mortar banking infrastructure can only provide so many dollars to the people. Tokenizing US Dollars and issuing them on public blockchains removes the current infrastructure related bottle neck of dollar issuance and makes access to US dollars significantly easier for billions of people across the globe. The dollar is the world’s reserve currency and savers worldwide covet the currency’s relative stability. By relying on a new public blockchain infrastructure, stablecoins can penetrate markets where banks refuse to participate. Stablecoin adoption is a tailwind for demand and strength of the US Dollar.

Blockchain technology has unlocked a currency competition unlike any that we have ever seen. There are currently ~180 currencies, 60 of those currencies are pegged to the US Dollar. How many of those not pegged to the dollar will be able to compete in a world where citizens across the globe have the choice and access to receive their currency of choice - a digital dollar? In addition to global adoption, another component to keep an eye on is if and when the use of stablecoins transition from purely a trading use case to broader transaction uses cases (i.e., eccommerce). Widespread use could result in declining transaction revenues and data capture for incumbent payment processors and the emergence of non-traditional payments platforms (i.e., big tech - FB, Google, Amazon are each working on various stablecoin or blockchain related initiatives)

Who did what this month?

Flushing Bank, a New York State-chartered commercial bank, will offer Bitcoin services to its customers in Q1 2022. Customers will soon be able to buy, sell, and hold bitcoin directly within their online banking accounts Link.

Former a16z crypto partner Katie Haun is raising nearly $900 million for her new venture firm, KRH. Haun is raising two funds, including a $300 million early-stage fund and another $600 million fund that will invest in larger companies and tokens. Link.

PayPal Is Exploring Creating Its Own Stablecoin as Crypto Business Grows: PayPal (PYPL) is looking into launching its own stablecoin as the company grows its crypto business Link

Novi, the crypto wallet owned by Meta (fka Facebook), has launched a small pilot on WhatsApp. Users can send/receive money directly in app. Link.

NY Fed Launches Fintech Research Wing With BIS Help: The Federal Reserve Bank of New York launched the New York Innovation Center (NYIC) to build and test new financial technology, including central bank digital currencies (CBDC), stablecoins and cross-border payments Link.

a16z is raising $4.5 billion for new crypto funds, including $1 billion for seed investments in web3. Link.

Rio de Janeiro mayor plans to invest 1% of the city's treasury in bitcoin. Link.

FTX is launching a $2 billion venture fund, FTX Ventures. Amy Wu from Lightspeed will lead the new fund. Link.

BlackRock Looks to Enter Crypto ETF Arena With Blockchain Fund - Blockworks. Link.

A new survey from E&Y showed that one third of hedge fund managers, 24% of alts investors, and 13% of PE managers plan to add crypto to their portfolios over the next 1-2 years. Only 7% said they already have crypto-related assets in their portfolios. Link. Link.